We aim to spearhead the energy transition in West Africa by achieving the highest levels of operational and emissions efficiency. Our approach involves developing a substantial and varied non-operated and operated portfolio of mid-life producing assets, which offers opportunities to enhance production and lower emissions.

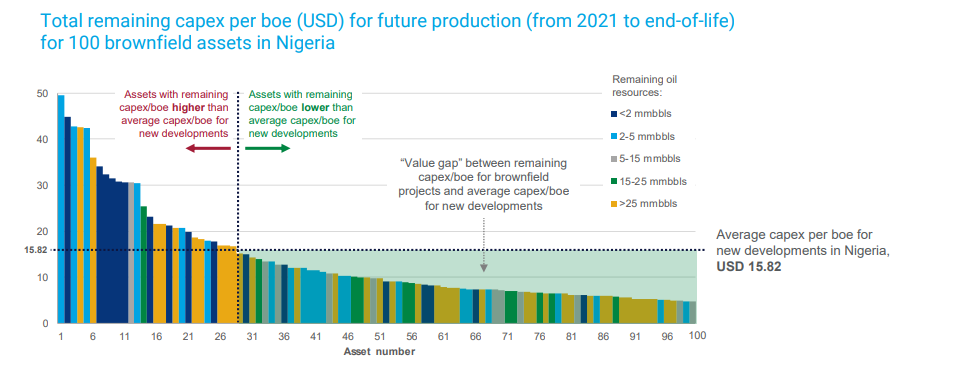

We estimate that the top 20 potential opportunities have a total remaining pre-tax valuation of $52bn and a total remaining post-tax valuation of $7.1bn (Wood Mackenzie)

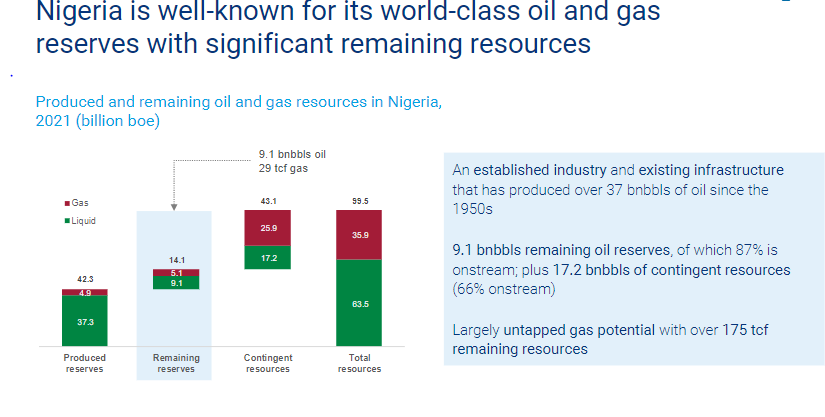

Nigeria stands as Africa’s leading oil producer with a well-established oil and gas industry dating back to the 1950s. In 2020 Nigeria achieved a daily average production of 1.9 million barrels of liquids and 4.6 billion cubic feet (bcf) of sales gas from over 220 fields operated by around 160 entities. Additionally, over 260 companies have upstream interests in the country. However, international oil companies (IOCs) are increasingly shifting their focus towards energy transition, resulting in reduced investment in their Nigerian portfolios.

The recent surge in oil prices and improved capital discipline have significantly enhanced project economics. With world-class reserves of approximately 9.1 billion barrels of oil and 29 trillion cubic feet (tcf) of gas, Nigeria presents compelling brownfield investment opportunities at both the asset and corporate levels, such as project financing and OML farm-ins.

The Nigerian government is dedicated to the development of marginal fields, which are primarily located onshore, in swamp areas, and in shallow waters. According to the Nigerian Government, a marginal field is a discovered resource that has been left undeveloped for over ten years. Many of these fields, previously held by Shell, ExxonMobil, Chevron, and Total, remain untapped, with only a few having been appraised. The total resources available for investment are estimated to be around 800 million barrels (mmbbl) of oil and 4.5 tcf of gas. The 25 largest oilfields alone could attract $9.4 billion in investment within the first five years and generate over $38 billion in revenue throughout their lifespan.

Augere Energy is strategically focused on acquiring high-value, under-invested assets with significant volume potential. Our goal is to build a diverse portfolio of mid-life producing assets that provide substantial opportunities for optimizing production processes and reducing emissions. We are particularly focused on low-risk appraisal and development projects within the prolific West African region, known for its abundant hydrocarbon deposits.

By leveraging these opportunities, Augere Energy aims to enhance production efficiency and support sustainable energy development in Nigeria. Our approach includes the integration of advanced technologies and innovative practices to maximize output while minimizing environmental impact.

Despite the profitability of their Nigeria assets, the IOCs are under increased pressure to accelerate their energy transition and divest non-core assets( Wood Mackenzie)

In addition to optimizing production, we are dedicated to reducing emissions through the adoption of greener technologies and processes. This dual focus on efficiency and sustainability aligns with global energy trends and positions Augere Energy as a leader in the responsible development of Nigeria's vast energy resources.

Our strategy is supported by strong partnerships with key stakeholders, including national oil companies, financial institutions, and technical experts. These collaborations ensure we have the necessary resources and support to achieve our ambitious goals.